As we’ve seen in our previous posts, timing the market is an almost impossible feat to perform. We’ve demonstrated that the risks involved in market timing can be large in terms of failing to meet your financial goals.

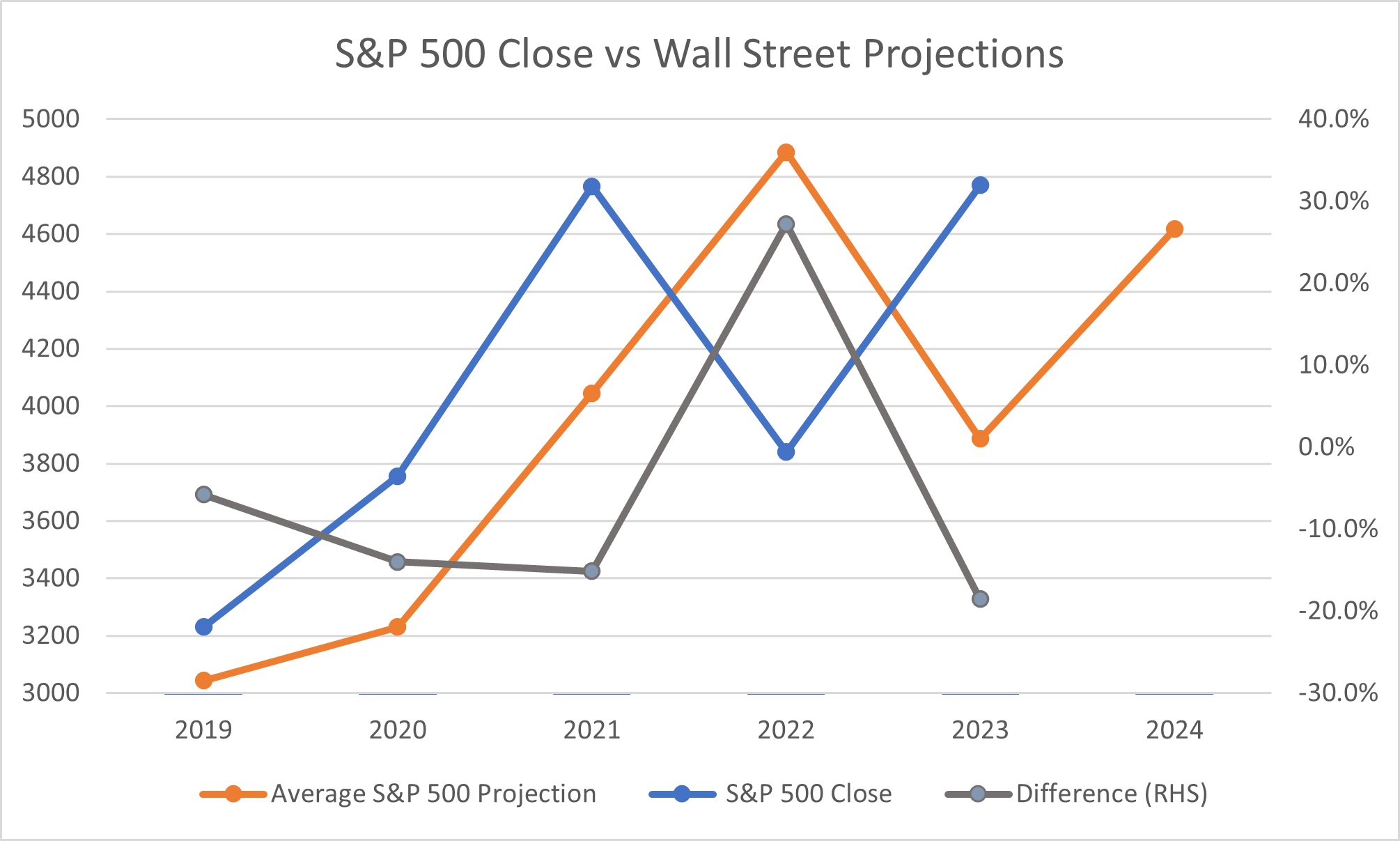

If you want to start investing today, you might think it is worthwhile to look at what Wall Street (the supposed pros) are thinking of for 2024, and their track record:

(Source: Bloomberg, projections taken from 12 banks)

Not only have the brightest minds in Wall Street missed the mark by at least 5% each year, but the projections seem to be worsening over time!

Now for one who is about to start investing, you might be thinking – if the supposed best minds can’t predict it consistently, you might be better off by staying invested. And to do that, you need to deploy your capital. How then can you invest in a ‘timing-neutral’ manner? Here we evaluate two methods of deployment:

Investing all your available money at once – if you have $1,000 to invest into S&P 500 at the start of 2023, you will buy $1,000 of S&P 500 on Jan 1. This means you are fully deployed on day 1.

Investing your money over time – Instead of going “all in”, for each month, you will buy $100 of S&P 500 on a set date each month. For an investment budget of $1,000, this means you will be fully invested by Oct 2023.

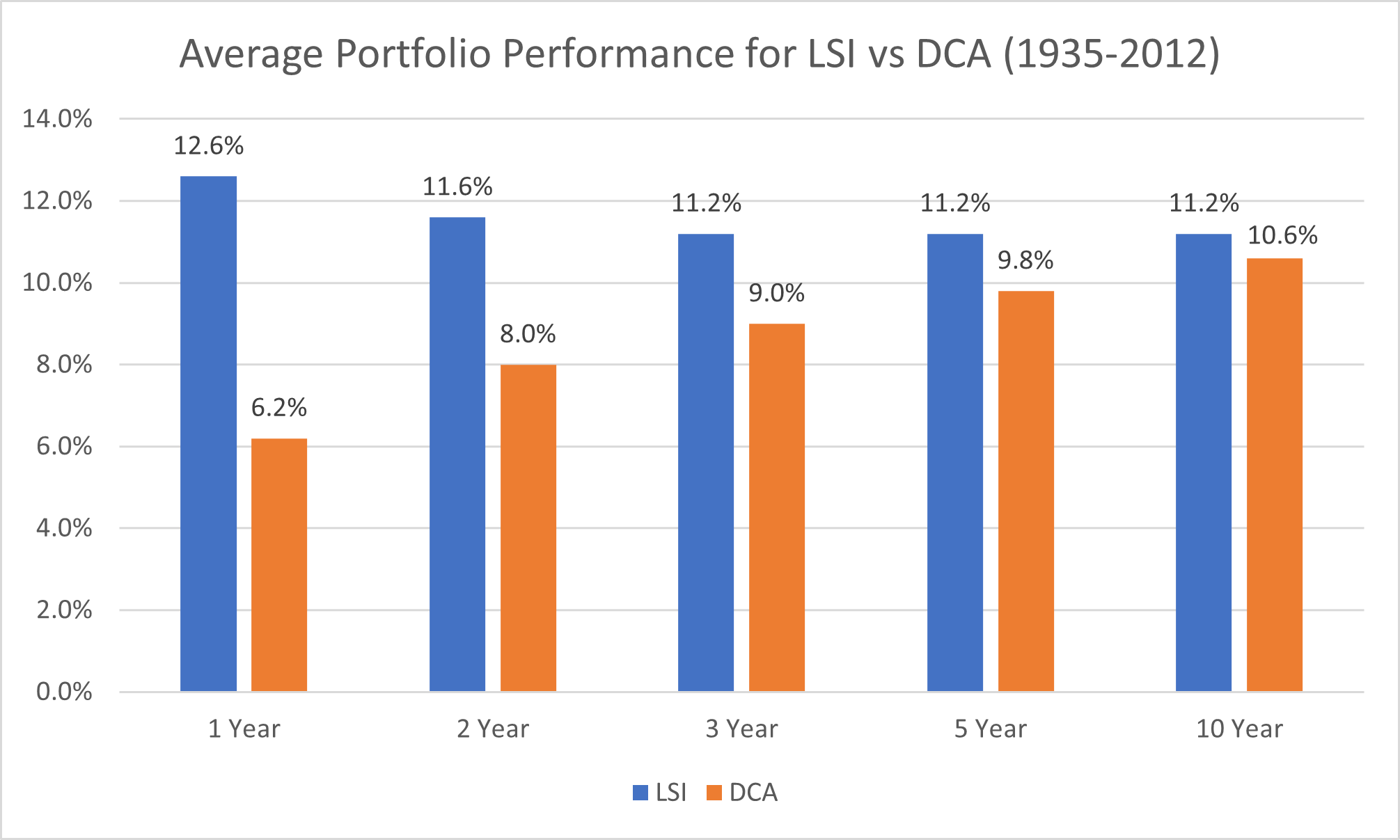

Case study: LSI or DCA?

Let’s reference a study done by Partner’s Capital, who simulated returns for an S&P 500 portfolio invested according to LSI or DCA for every month from January 1935 to January 2012.

For LSI, the portfolio is fully invested on day 1.

For DCA, the portfolio is deployed across two years at quarterly intervals with equal quantum. Uninvested balances were held in cash. This presents 936 monthly “entry points”, a rich array of data:

(Source: Partner’s Capital – Portfolio Deployment)

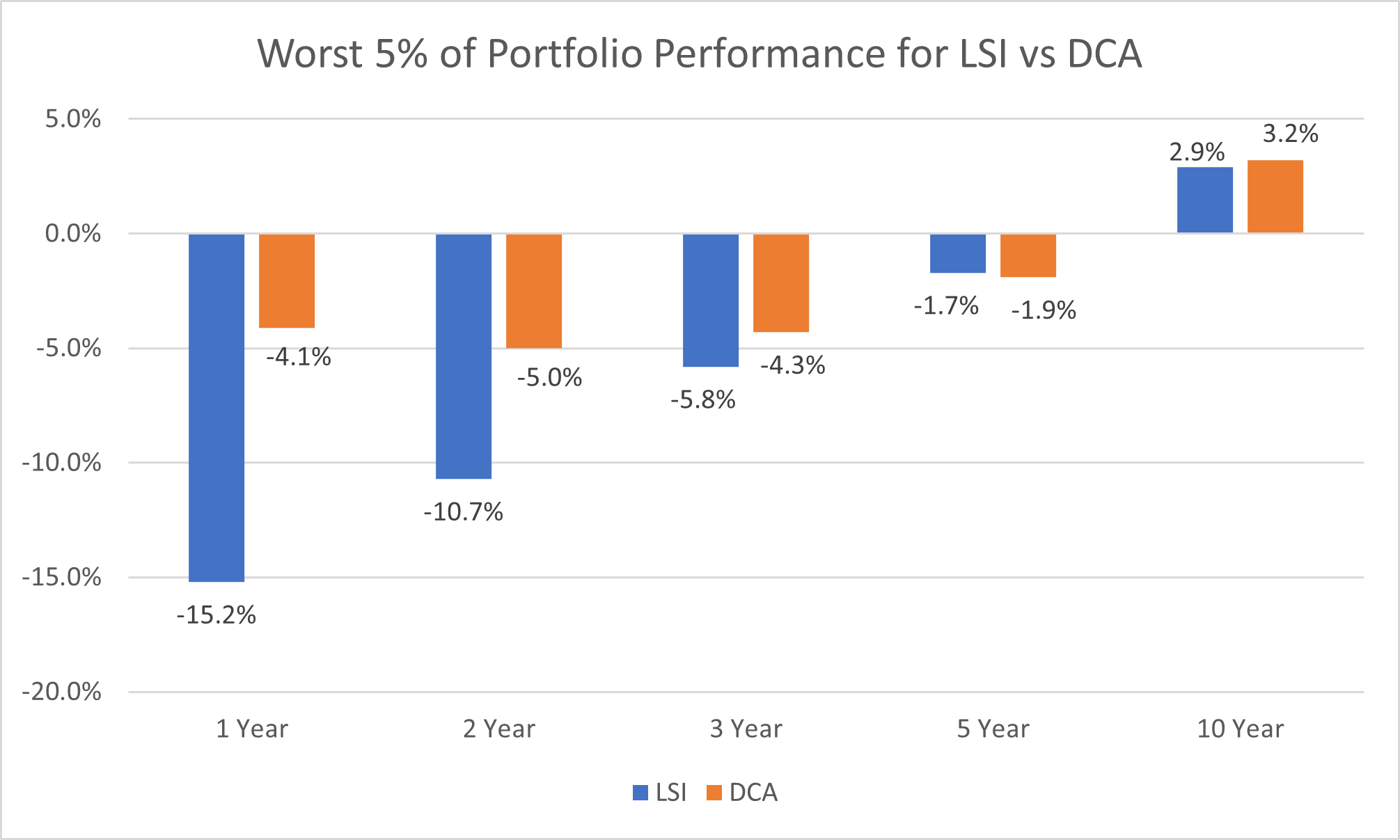

The results show that the LSI approach does produce a higher average return across all time periods. However, it does come with risks:

Within 1 – 3 year time periods, the worst 5% of outcomes for the LSI portfolio are more severe than DCA portfolios. From 5 years onwards, the disparity in outcomes reduces. The results are intuitive: over any time period, a fully invested portfolio of equities outperforms a partially invested portfolio of equities and cash (stay invested!). The only periods when DCA outperformed LSI were when there were significant market drawdowns.

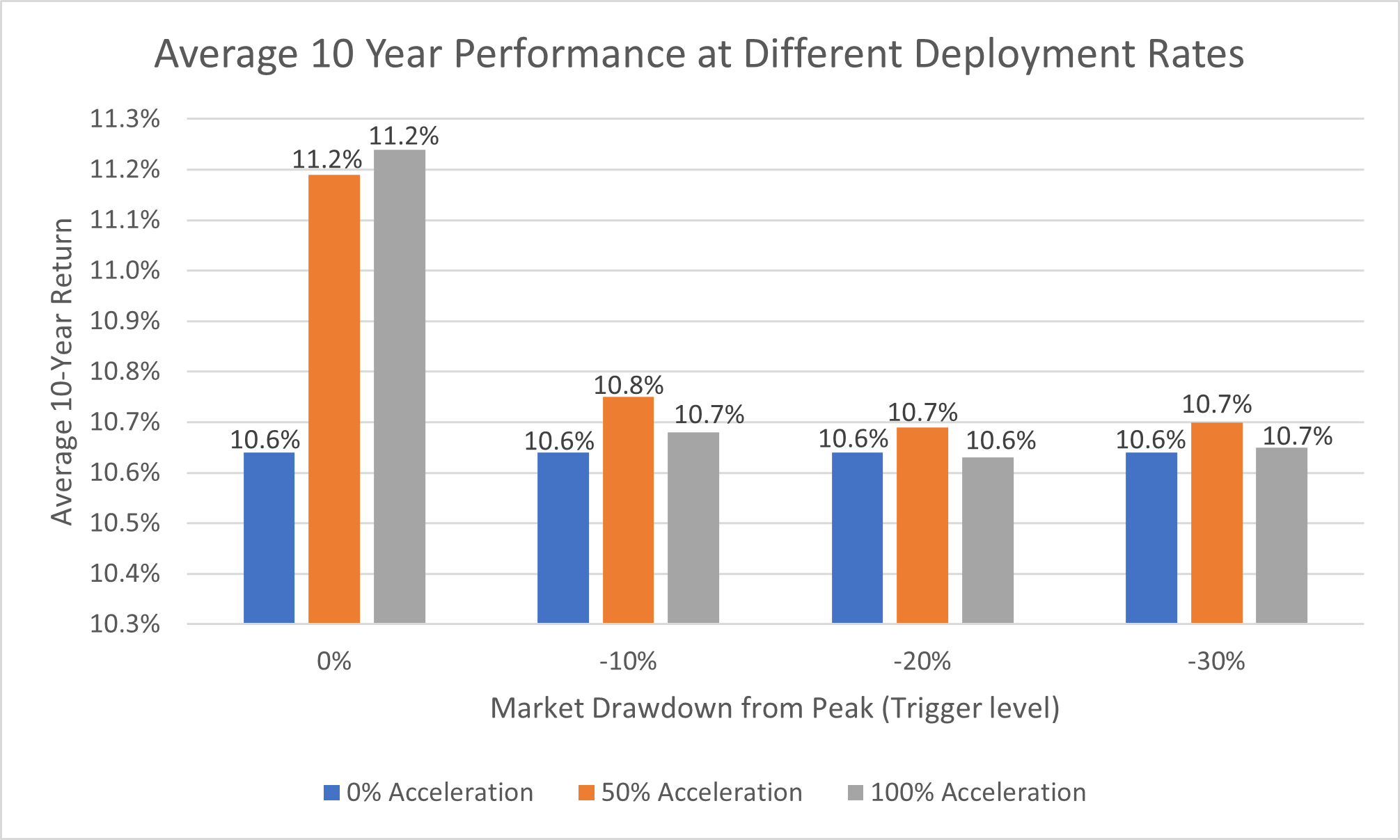

Wait, you might be thinking – during drawdowns, there might be some element of market timing that allows one to consistently produce better returns via DCA. By accelerating the deployment plan at different trigger points (drawdown levels), one can achieve better ten-year average returns. For example, if you have 10 months left to fully deploy and the market draws down by 10% from its peak, and you can accelerate deployment by 100% (deploying the rest within 5 months). Testing it across different triggers and acceleration rates, this hybrid method does produce better results:

The baseline 10.6% return (no acceleration) is outperformed by accelerating the deployment rate across almost all market drawdown events.

What works for you?

The decision to use LSI or DCA depends on your risk appetite and loss aversion. Individuals who sleep well in times of volatility can consider the LSI approach, whereas investors who are more sensitive to drawdowns should consider the DCA approach. During drawdown periods, they can even pick up the pace of deployment to get more bang for their buck. And there you have it – a way to ‘time’ the market.

NOTICE TO VISITORS TO OUR WEBSITE: Javelin Wealth Management is aware of a recent instance of our website being fraudulently duplicated (“cloned”) and used to promote property investment products in Germany. Javelin Wealth Management has notified the relevant authorities of this, and would like to emphasize that Javelin Wealth Management has no connection with any such products, or with the company calling itself “Wing-wealth”. Our website is not used to promote specific investment products and does not carry any customer data. Investors should always confirm that they are dealing with properly licensed and regulated individuals and entities, and should check with their local regulatory body in the event of any doubt.

By entering this site, you agree to be bound by the following Terms and Conditions of Use.

Javelin Wealth Management Ptd Ltd, holder of Capital Markets Services Licence, is licensed by the Monetary Authority of Singapore to provide Fund Management Services to individuals who are Accredited Investors.

Accredited & Professional Investors

By using this site you represent and warrant that you are an accredited and professional investor as defined in Section 4A(1)(a) of the Securities and Futures Act with personal net assets in excess of S$2 million, income in the preceding 12 months of not less than S$300,000, or company net assets in excess of S$10m. In using this site the user represents that they are an accredited and/or professional investor and use this site for their own information purposes only.

Information Purposes Only

The information published on this site is for informational purposes only and shall not be construed as an offer or solicitation to subscribe in the funds or products referred herewith. This site does not constitute investment advice or counsel or solicitation for investment in any fund.

Any offer or solicitation will be made only upon execution of completed information memorandum, subscription application and relevant documentation, all of which must be read in their entirety. No offer to subscribe in shares will be made or accepted prior to receipt by the offeree of these documents and the completion of all appropriate documentation. Access to information about the funds is limited to investors who qualify as accredited investors only.

Any projections or forward looking statements are not necessarily indicative of future or likely performance. Past performance is no guarantee of future performance of a fund.

Conditions of Use

I have read and accept the terms and condition of use.